Freelancer or self-employed

The differences between a freelancer and a self-employed person, and what each means for you.

Read moreLog in to your account, or sign up in a minute.

Pick whatever works for you · we're here.

Everything about NETO · transparent and available

Pick a convenient time · we'll confirm by phone/email

The difference between self-employed and salaried under Israeli National Insurance is more nuanced than it seems · the institute has its own criteria, which sometimes differ from the definitions in the law. Here we have gathered the definitions, the brackets, the rates and the criteria · clearly, so you know exactly where you stand.

Who is salaried and who is self-employed under National Insurance?

A salaried worker under National Insurance is anyone in an employer-employee relationship with their employer, or anyone who meets the definitions in the insured-classification and employer-determination order. A self-employed person is anyone for whom no employer-employee relationship exists. If only it were that simple · in practice the institute has its own criteria, which sometimes differ from the definitions in the law, and it assesses each case under the mixed test and the classification order.

In brief: a salaried worker pays national insurance contributions across two brackets (3.5% and 12% from the employee), and at times a self-employed person too is treated as an employee for entitlement purposes. A self-employed person is treated as such in the tax year based on work-hour and income tests. Note · not everyone defined as salaried is automatically entitled to National Insurance benefits.

This article explains how self-employed and salaried are defined under Israeli National Insurance. The answer is complex and far from simple · we will try to address the questions and clarify the matter. Note that the National Insurance definitions sometimes differ from the definitions in the law, and the institute applies its own criteria to determine who is salaried and who is self-employed.

Anyone for whom an employer-employee relationship exists · that is, there is a worker-employer bond, assessed by tests established in case law.

Anyone for whom no employer-employee relationship exists. Yet here too, the institute adds work-hour and income tests to determine who is in fact treated as self-employed.

Important: not everyone defined as salaried is in fact salaried for National Insurance purposes · even if the employer defined them as salaried and paid national insurance contributions on their behalf. To receive the benefits that contributions fund, you must meet the National Insurance criteria.

The definition of salaried is anchored in law. Under the definition developed through extensive case law, the situation must be examined by the mixed test · which weighs several parameters to assess an employer-employee relationship. Every salaried worker in Israel who meets the National Insurance criteria is entitled, on one hand, to a range of social and pension benefits, and on the other hand to National Insurance benefits (such as unemployment, unpaid-leave allowances and so on).

Every salaried worker pays taxes on their gross income, including national insurance contributions according to the brackets set in law. Under the National Insurance definition, there are in total two brackets for calculating contributions · detailed below.

A salaried worker under the National Insurance definition is one of the following:

Anyone in an employer-employee relationship with their employer.

Anyone who meets the definitions in the insured-classification and employer-determination order (see below).

The National Insurance (Classification of Insured Persons and Determination of Employers) Order, 5732-1972. The order's purpose is to broaden National Insurance coverage · that is, under certain conditions a self-employed person will be treated as an employee for entitlement purposes.

There are cases where a self-employed person is treated as an employee. When? When the insured person performs work listed in column A of the First Schedule, but only if they work under the special conditions set out beside it in column B. If both criteria are met (column A and column B), the self-employed person is treated under the law as an employee.

Who is deemed the employer of that "self-employed" person holding an employee's rights? The employer of a worker is deemed to be the party specified beside them in column C of the First Schedule.

An insured person who performs work as set out in column A of the Second Schedule, and works under the special conditions set out beside it in column B, is treated under the law as a self-employed worker · provided they meet the conditions of the definition of a self-employed worker in section 1 of the law.

An insured person engaged in the activity set out in the Third Schedule is treated under the law, during that activity, as one who is neither an employee nor a self-employed worker.

A concise comparison between the two statuses under National Insurance · based on the facts in this article:

| Parameter | Salaried | Self-employed |

|---|---|---|

| Basic definition | An employer-employee relationship exists, or meets the classification order | No employer-employee relationship exists |

| Governing test | The mixed test · weighs parameters of an employer-employee relationship | Weekly work-hour and average monthly income tests |

| Income basis | Gross income · according to the brackets set in law | Annual income · attributed to the period of activity in the tax year |

| First bracket | 3.5% from employee + 3.55% from employer (7.05% combined) up to ILS 6,331 | Determined by the person's occupation status and income |

| Second bracket | 12% from employee · from ILS 6,331 up to the max ILS 45,075 | Determined by the person's income |

| Automatic entitlement | Not necessarily · you must meet the National Insurance criteria | Assessed by meeting the conditions of the self-employed definition |

| Possible benefits | Unemployment, unpaid-leave allowances, social and pension benefits | According to self-employed status and the applicable entitlements |

National insurance and health contribution rates for salaried workers who are Israeli residents, aged 18 up to retirement age · as a percentage of the wage (effective from 01.01.2022):

From the first shekel up to 60% of the average wage · that is, ILS 6,331. On all income up to this bracket's ceiling, 3.5% is contributed toward national insurance and health. The employer also contributes 3.55% against the employee · a combined 7.05%.

All income above ILS 6,331 and up to the maximum income liable for contributions · ILS 45,075. If income exceeds this amount, 12% is deducted from the employee's funds toward national insurance and health contributions.

The maximum income liable for contributions is ILS 45,075. Beyond this ceiling, no further national insurance and health contributions are deducted from the wage.

A self-employed person who does not meet the definition, who becomes self-employed during the year or vice versa · how is their income spread out in the eyes of National Insurance? For example: a self-employed person who does not meet the definition until the end of April, and from May does meet it, or the other way around.

Income from a self-employed source is annual income, and it is attributed to the period of activity (in which the person meets or does not meet the definition) within the tax year. Accordingly, a person's occupation is defined as self-employed in the tax year when they meet one of the following conditions:

Works as self-employed at least 20 hours a week on average.

Average monthly income equals or exceeds 50% of the average wage · ILS 5,276 (effective from 01.01.2020).

Works as self-employed at least 12 hours a week on average, and average monthly income is not below 15% of the average wage · ILS 1,583 (effective from 01.01.2020).

Everything stated above is neither advice nor authoritative reference · it is advisable to consult a professional such as a tax advisor, accountant, or attorney specializing in labor law and securing rights. For support and customer service · +972-8-976-1874.

A salaried worker under the National Insurance definition is anyone in an employer-employee relationship with their employer, or anyone who meets the definitions in the insured-classification and employer-determination order. Note that not everyone defined as salaried is automatically entitled to benefits · you must meet the National Insurance criteria.

A self-employed person is anyone for whom no employer-employee relationship exists. They are treated as self-employed in the tax year if they work at least 20 hours a week on average, or their average income equals or exceeds 50% of the average wage (ILS 5,276), or they work at least 12 hours a week and their income is not below 15% of the average wage (ILS 1,583).

First bracket · up to ILS 6,331, 3.5% is deducted from the employee and the employer adds 3.55% (7.05% combined). Second bracket · on income above ILS 6,331 and up to the maximum ILS 45,075, 12% is deducted from the employee for national insurance and health contributions.

The National Insurance (Classification of Insured Persons and Determination of Employers) Order, 5732-1972 · its purpose is to broaden National Insurance coverage so that, under certain conditions, a self-employed person is treated as an employee for entitlement purposes. If an insured person performs work in column A and works under the conditions in column B of the First Schedule · they are treated under the law as an employee.

Not necessarily. Not everyone defined as salaried is in fact salaried for National Insurance purposes · even if the employer paid national insurance contributions on their behalf. To receive the benefits, you must meet the National Insurance criteria, assessed under the mixed test.

Under the classification order · when the insured person performs work listed in column A of the First Schedule, and only if they work under the special conditions set out in column B. If both conditions are met · the self-employed person is treated under the law as an employee, and their employer is determined under column C.

NETO lets you work and issue a lawful invoice · without opening a tax file and without the hassle with National Insurance. Fast, free signup.

The differences between a freelancer and a self-employed person, and what each means for you.

Read more

When such a relationship is formed, the mixed test, and what it means for your rights.

Read more

How much is deducted from a salaried worker, by which brackets, and what it means for your payslip.

Read moreYou can be both salaried and self-employed · how it works and what to know.

Read moreWhat a worker in Israel is entitled to · social, pension and National Insurance benefits.

Read moreThe differences between a freelancer and a self-employed person, and what each means for you.

Read moreWhen such a relationship is formed, the mixed test, and what it means for your rights.

Read moreHow much is deducted from a salaried worker, by which brackets, and what it means for your payslip.

Read moreYou can be both salaried and self-employed · how it works and what to know.

Read more YC

YCEvery section, organized by topic. Browse the full hierarchy or jump straight in.

Adjust the site to your needs

We use cookies to run the site and, with your consent, to measure traffic and improve your experience. Privacy policy

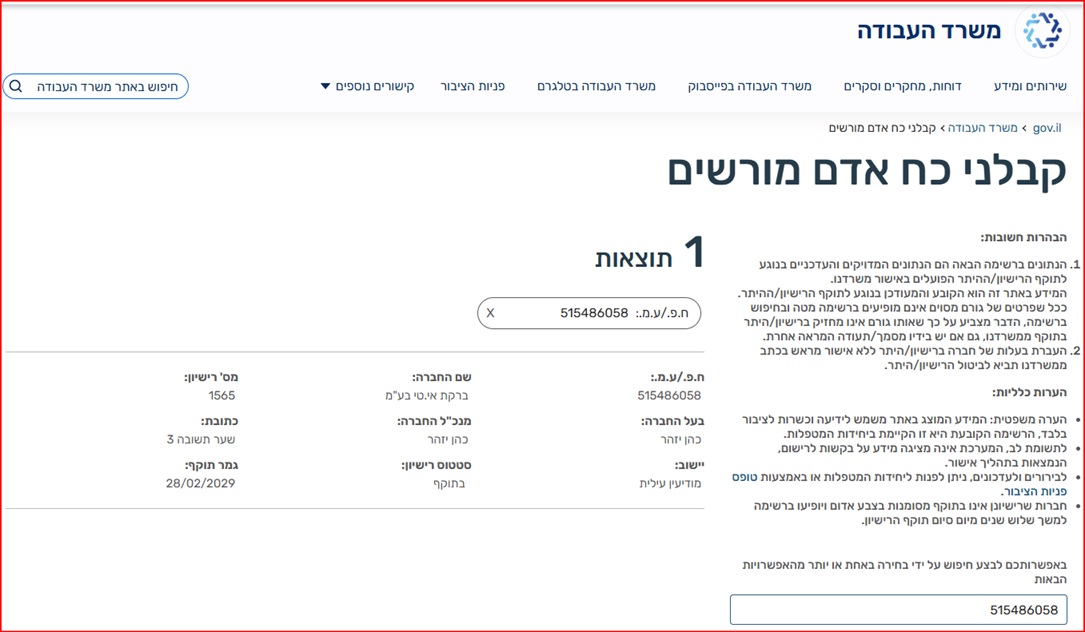

ברקת אי.טי בע״מ · בשם המותג NETO · היא חברת כוח אדם בעלת רישיון 1565 ומפוקחת על ידי משרד העבודה.

אימות הרישיון באתר משרד העבודה

למידע המלא · דף רישיון קבלן כוח אדם ←

אימות הרישיון באתר משרד העבודה

למידע המלא · דף רישיון קבלן כוח אדם ←