Employee Pension Contributions in Israel – The Complete Employer Guide 2026

Mandatory pension contributions apply to every employer in Israel · no exceptions. This comprehensive 2026 guide covers contribution rates, the salary ceiling, Section 14, penalties, Appendix V, and how NETO handles full compliance on your behalf as your Employer of Record.

AI Summary Smart overview of this page · click here

Employee pension contributions in Israel are a legal obligation · not optional. Under the Extension Order for Comprehensive Pension Insurance (in force since 2008), every salaried employee over age 21 (male) or 20 (female) is entitled to pension contributions, regardless of company size or type of position. The 2026 rates: 6% employee, 6.5% employer pension and 6% severance · up to 15% employer and up to 21% total. The obligation applies retroactively from the first day of employment, after a waiting period of 6 months (no prior insurance) or from day one (with existing insurance). Non-compliance means fines of up to NIS 35,000 per violation, lawsuits and retroactive payments. NETO, a licensed manpower contractor (#1565), acts as your Employer of Record and contributes per Section 14 (6% + 6.5% + 8.33% severance) · accurately, on time and in full compliance.

This summary is generated from the page content and the linked sources · full detail below. It is not legal advice.

Guide Summary

Everything you need to know about employee pension contributions in Israel · the essential guide for every employer, in brief:

- Every salaried employee is entitled to pension contributions · without exception*.

- Full contribution rate: up to 21% (6% employee + up to 15% employer).

- The obligation applies retroactively from the first day of employment.

- Non-compliance means breaking the law · fines and lawsuits.

* There are exceptions: employees under age 21 (male) / 20 (female), employees without an active pension fund during the waiting period, and more. See details below.

Table of Contents

- What Does Israeli Law Say? The Extension Order for Mandatory Pension

- Who Is Eligible?

- The Waiting Period · When Do Contributions Begin?

- Updated Rates 2026

- Annual Ceiling 2026

- How Much Do Pension Contributions Cost?

- Sanctions and Risks

- Which Pension Funds Can You Contribute To?

- Appendix V · Employee's Choice of Fund

- Section 14 of the Severance Pay Law

- Employee Declaration

- The NETO EOR Solution

- Frequently Asked Questions

- Summary

Israel pension contributions 2026 · key figures

What Does Israeli Law Say? The Extension Order for Mandatory Pension

Understanding employee pension contributions in Israel is essential for every employer. Since 2008, Israel has enforced the Extension Order for Comprehensive Pension Insurance (under the Collective Agreements Law, 5717-1957). This landmark legislation established that every salaried employee in Israel is entitled to pension contributions · regardless of the size of the business, the type of position (full-time or part-time), or the nature of the employment.

In other words, employee pension contributions in Israel are mandatory · even if you have only one employee, you are legally obligated to contribute on their behalf. Full detail of the mandatory pension obligation appears on Kol Zchut · mandatory pension insurance.

Employee Pension Contributions Israel – Who Is Eligible?

Every salaried employee over the age of 21 (male) or 20 (female) is entitled to pension contributions, including:

- Full-time and part-time employees

- Temporary and seasonal workers

- Employees in their probation period (after the waiting period)

- Remote workers (work from home)

- Foreign employees (subject to certain conditions)

The Waiting Period – When Do Contributions Begin?

According to the Extension Order, the obligation to contribute begins as follows:

After 6 months of employment at the same workplace, retroactively from the first day of work.

From the first day of work, with actual contributions beginning after 3 months or at the end of the tax year (whichever comes first), retroactively.

Employee Pension Contributions Israel – Updated Rates 2026

Below are the current employee pension contributions Israel rates as mandated by law for 2026:

| Component | Employer Share | Employee Share | Total |

|---|---|---|---|

| Pension (Tagmulim) | 6.5% | 6% | 12.5% |

| Severance (Pitzuyim) | 6% | · | 6% |

| Disability Insurance* | Up to 2.5% | · | Up to 2.5% |

| Maximum Total | Up to 15% | 6% | Up to 21% |

* Disability insurance (loss of work capacity) is included within the employer's 6.5% contribution, but coverage varies depending on the fund type and policy terms.

At NETO we deposit for the employee according to Section 14: 6% employee Tagmulim + 6.5% employer Tagmulim + 8.33% severance.

Employee Pension Contributions Israel – Annual Ceiling 2026

Israeli law sets a maximum salary amount on which mandatory pension contributions are calculated. Under the Extension Order this ceiling is tied to the average wage in the economy, updated each January by the National Insurance Institute.

For 2026, the average wage in the economy · and therefore the ceiling for mandatory pension contributions · is approximately NIS 13,316 per month. Salary earned above this amount is not subject to mandatory pension contributions, although many employers choose to contribute on the full salary for the benefit of the employee.

| Parameter | Value 2026 |

|---|---|

| Average wage in the economy | ≈ NIS 13,316 (updated each January) |

| Ceiling for mandatory contributions | ≈ NIS 13,316 |

| Maximum employer contribution (15%) | ≈ NIS 1,997 / month |

How Much Do Pension Contributions Cost? A Calculation Example

Let's look at a practical example for an employee earning NIS 10,000 gross per month:

| Component | Rate | Monthly Amount (NIS) |

|---|---|---|

| Employer – Pension (Tagmulim) | 6.5% | 650 |

| Employee – Pension (Tagmulim) | 6% | 600 |

| Employer – Severance (Pitzuyim) | 8.33% | 833 |

| Total Employer Cost | 14.83% | 1,483 |

| Total Deposited to Fund | 20.83% | 2,083 |

Employee Pension Contributions Israel – Sanctions and Risks

Failing to make pension contributions is a violation of Israeli labor law and can result in severe consequences:

Fines of up to NIS 35,000 per violation, imposed by the National Insurance Institute and the Ministry of Labor.

Employees can sue for the full amount of unpaid contributions, plus interest and linkage differentials.

In extreme cases, willful non-compliance can lead to criminal proceedings.

You'll need to pay all missing contributions retroactively, often with penalties.

Labor court verdicts are public record and can harm your ability to recruit.

Which Pension Funds Can You Contribute To?

In Israel, pension contributions can be deposited into several types of savings instruments:

Keren Pensia Makifa · the most common option, offering pension, disability and survivors' benefits.

Kupat Gemel · a savings-oriented fund without insurance components.

Bituach Menahalim · an insurance-based pension product (less common for new policies since 2013).

Appendix V (Nispach Vav) – Employee's Choice of Pension Fund

Every employee has the right to choose their own pension fund. To enable the employer to deposit contributions into the employee's preferred fund, the employee must provide an Appendix V (Nispach Vav) form.

What Is Appendix V?

Appendix V is an official form issued by the insurance company or pension fund. It serves as confirmation from the fund to the employer that the employee has an active pension account and authorizes the employer to make deposits into it.

How to Obtain Appendix V

The employee should contact their insurance company or insurance agent and request the form, which should include the following employer details:

Consequently, we deposit pension contributions on the employee's behalf according to Section 14 of the Severance Pay Law: 6% employee + 6.5% employer pension + 8.33% severance.

The Four Selected Default Pension Funds

| Pension Fund | ID Check Digit |

|---|---|

| Altshuler Shaham | 2, 3 |

| Meitav | 0, 1 |

| Infinity | 7, 8, 9 |

| Mor | 4, 5, 6 |

How is the fund selected? Starting June 2025, for employers with 50 or more employees, the fund assignment is determined by the check digit (last digit) of the employee's Israeli ID number. Smaller employers may select any of the 4 funds. Maximum management fees: 0.22% of the accumulated balance + 1.00% of deposits · fixed for at least 10 years, with no medical questionnaire or underwriting.

Section 14 of the Severance Pay Law

Section 14 of the Severance Pay Law (1963) is a crucial provision for both employers and employees. It establishes that ongoing pension contributions made by the employer count toward the severance pay obligation. In practice this means:

- When an employer contributes at least 8.33% of salary to a severance component in a pension fund, those contributions replace the obligation to pay full severance upon termination.

- The money belongs to the employee from the moment it is deposited.

- The employer is released from additional severance liability for the amounts already contributed.

- This provides certainty for both parties and simplifies the employment relationship.

At NETO, we apply Section 14 for all employees · contributing 6% employee + 6.5% employer pension + 8.33% severance, ensuring full compliance and financial clarity for both the employer and the employee. See more on the Severance Pay Law in Israel.

Employee Declaration – Regarding Pension Contributions

In certain circumstances, an employee may request that the employer not make pension contributions on their behalf. This applies mainly in two situations: the employee does not have an active pension and compensation fund (in the last 6 months), or the employment is a one-time job or lasts less than two months. In such cases, the employee must sign a formal declaration accepting responsibility for not receiving pension contributions.

View the employee / freelancer declaration wording

The employee's / freelancer's statement · regarding the deposit for pension and compensation

I hereby declare that: I know and understand the law regarding the employer's responsibility for depositing into the pension fund and compensation. And so I state that:

- I do not have an active pension and compensation fund (in the last 6 months).

- This is a one-time job/transaction and/or the period of the job/transaction will be less than two months.

Therefore, I request that NETO · Bareket IT Ltd. will not deposit for me for pension and compensation. Rather, I will take the excess money that I earn by virtue of this statement and I myself will make sure to deposit it for the pension and compensation according to the law.

I undertake not to make any claims/demands towards NETO (Bareket IT Ltd.). If I am asked, it is my responsibility to immediately pay the pension money, the compensation, the fines and the differences retroactively.

It is clear to me that as a result of my statement my net income has increased, but the tax burden may increase. I confirm that it was explained to me that had I not made this statement, the pension funds and compensation would have been deposited for me with the insurance company (according to Section 14 of the law) as part of the employer's costs, while the net amount remaining in my bank account would have been smaller.

Identity number: _______ Phone ID: _______ Job number: _______

This is my declaration, this is my name and this is my signature: _______

Employee Pension Contributions Israel – The NETO EOR Solution

Managing pension contributions, calculating percentages, meeting deadlines, choosing the right funds and filing reports · all of these require specialized knowledge and constant attention. A small mistake can cost you dearly. When you hire employees through NETO as your Employer of Record (EOR), all employer obligations transfer to us:

On time and in full compliance with the law · Section 14, Appendix V and all the rest.

Pay slips, National Insurance and income tax withholding · all handled for you.

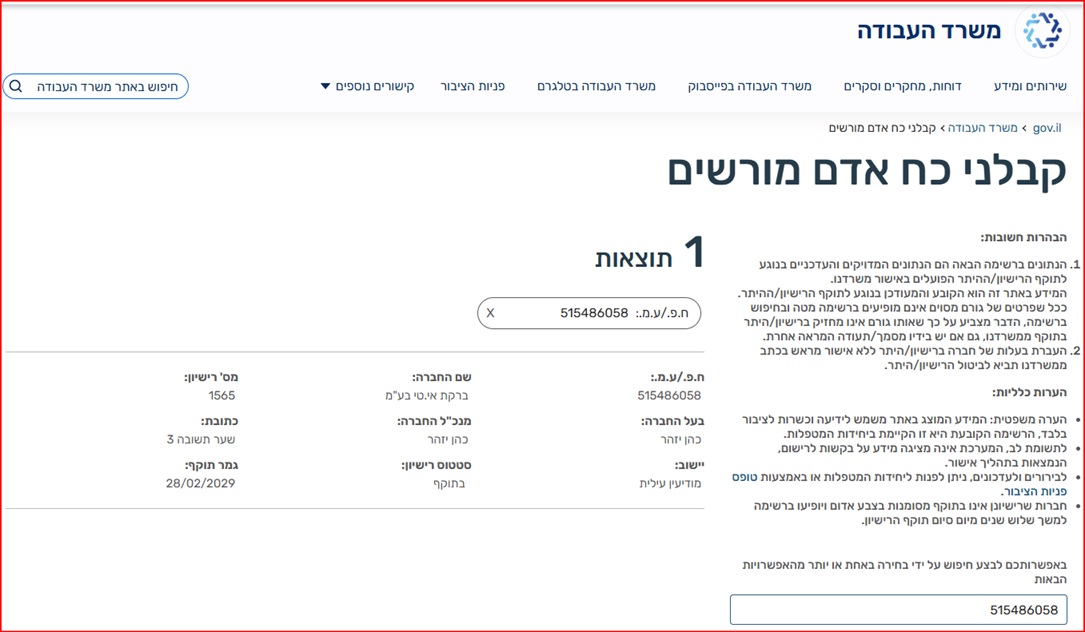

Lawsuits, fines and audits are on us, as the licensed legal employer (#1565).

Just like your own team · only without the bureaucracy. Learn more about NETO's EOR in Israel.

Frequently Asked Questions

Is an employer required to make pension contributions for a part-time employee?

Yes. Every salaried employee is entitled to pension contributions regardless of whether they work full-time or part-time. The contribution is calculated as a percentage of the actual gross salary paid.

When do pension contributions begin for a new employee?

For an employee with existing pension insurance · contributions begin from the first day, retroactively after 3 months or end of tax year. For an employee without prior pension · after 6 months, retroactively from day one.

Can an employee choose which pension fund to contribute to?

Yes. The employee has the full right to choose their pension fund. They need to provide an Appendix V (Nispach Vav) form from their chosen fund. If no choice is made within 60 days, the employer deposits into one of the government-selected default funds.

What is Section 14 and why is it important?

Section 14 of the Severance Pay Law allows employers to count ongoing pension contributions (at 8.33% of salary) toward their severance pay obligation. This means the employer is released from additional severance liability for amounts already contributed to the pension fund.

What are the penalties for not making pension contributions?

Non-compliance can result in fines of up to NIS 35,000 per violation, employee lawsuits for unpaid contributions plus interest, and in extreme cases criminal proceedings. All missing contributions must be paid retroactively.

How does NETO handle pension contributions as an EOR?

NETO serves as the legal employer (Employer of Record) and handles all pension contributions, payroll, tax withholding and compliance. We contribute according to Section 14: 6% employee + 6.5% employer pension + 8.33% severance, ensuring full legal compliance.

Are foreign companies required to make pension contributions for employees in Israel?

Yes. Any employee working in Israel is entitled to pension contributions under Israeli law, regardless of where the employer is based. Foreign companies often use an EOR service like NETO to ensure compliance with Israeli labor laws while hiring in Israel.

Summary

Pension contributions for employees in Israel are not optional · they are a legal obligation that applies to every employer. The total contribution can reach up to 21% of the gross salary (6% employee + up to 15% employer), and non-compliance carries severe penalties including fines, lawsuits and retroactive payments.

For international companies hiring in Israel, managing pension compliance can be complex. NETO offers a complete EOR solution that handles all employer obligations · from pension contributions and payroll to tax compliance and legal protection. Contact us today to learn how we can simplify your Israeli employment.

Last updated: 09/07/2026 · rates and figures are correct for 2026 and may be updated annually.

Ready to Hire in Israel with Full Compliance?

Let NETO handle the pension, payroll and legal complexity · so you can focus on your business. Register free for a payroll simulation, or ask us on WhatsApp.

Related guides worth reading

Employer of Record in Israel

Hire employees in Israel without a local entity · NETO is the legal employer.

Read more

Employer Cost in Israel

Salary, National Insurance, pension and severance · the full cost of hiring.

Read more

Severance Pay Law in Israel

How Section 14 works and what employers owe when employment ends.

Read more

Employee Rights in Israel

Minimum wage, vacation, sick pay, recuperation, pension and severance.

Read moreIsraeli Labor Law

Employee rights and employer obligations · the essentials in one place.

Read moreIsrael Payroll

Compliant local payroll, pay slips and reporting · run for you by NETO.

Read moreManpower Contractor License

Why licence #1565 matters · and how to verify it in the Ministry registry.

Read more