Self-employed vs salaried

How National Insurance defines each · the brackets, the criteria and what it means for you.

Read moreLog in to your account, or sign up in a minute.

Pick whatever works for you · we're here.

Everything about NETO · transparent and available

Pick a convenient time · we'll confirm by phone/email

A guide for salaried workers, freelancers and second earners · how much National Insurance and health contribution comes out of each payslip, who counts as salaried under the National Insurance Institute, the full rate brackets · and how, through NETO, even a freelancer without a tax file gets a payslip with everything already deducted lawfully.

Does a salaried employee pay National Insurance?

Yes. Every salaried employee in Israel pays National Insurance and health contributions from every payslip and on all income · large or small, sole or secondary. The deduction is taken at source from the gross wage: on income up to ILS 7,703 a reduced rate of 4.27% is deducted, and on every shekel above that the employee pays 12.17% (2026 figures).

This question is a little more involved, and on this page we answer it simply: what exactly comes out of the payslip and why, who even counts as a salaried worker in Israel under the National Insurance definitions, how it differs from a self-employed person · and what to do if you earn without a payslip at all. All rates follow the official National Insurance Institute figures and are marked with the year they refer to.

Two rates alone decide how much comes out of the payslip · according to the gross wage. The figures follow the National Insurance Institute, effective from 01.01.2026.

On income up to ILS 7,703 (60% of the average wage · 2026 figures) 4.27% is deducted from the employee toward National Insurance and health contributions. The employer adds 4.51% on top · a combined 8.78%.

On every shekel above that the employee pays 12.17% of the gross wage, up to the maximum income liable for contributions (ILS 51,910 · 2026 figures).

The example is illustrative and rounded · it applies the 2026 employee rates to a gross wage of ILS 10,000. Exact figures depend on your personal details; the National Insurance Institute provides an official contribution calculator.

Not everyone who is paid for work is automatically salaried. Under the National Insurance Institute definition there are two main criteria for being salaried:

National Insurance and health contribution rates for salaried workers who are Israeli residents, aged 18 up to retirement age · as a percentage of the wage, effective from 01.01.2026.

From the first shekel up to 60% of the average wage · that is, ILS 7,703. On all income up to this ceiling, 4.27% is deducted from the employee toward National Insurance and health contributions. The employer also contributes 4.51% · a combined 8.78%.

All income above ILS 7,703 and up to the maximum liable income · ILS 51,910. On income in this bracket, 12.17% is deducted from the employee toward National Insurance and health contributions.

The maximum income liable for contributions is ILS 51,910. Beyond this ceiling, no further National Insurance and health contributions are deducted from the wage.

A self-employed person, by contrast, manages these payments themselves directly with the National Insurance Institute and pays across their own brackets according to income · see the full picture in self-employed vs salaried under National Insurance and in freelancer or self-employed.

For a salaried employee, the whole process happens without them lifting a finger · the employer handles it on the payslip and in the report to the National Insurance Institute.

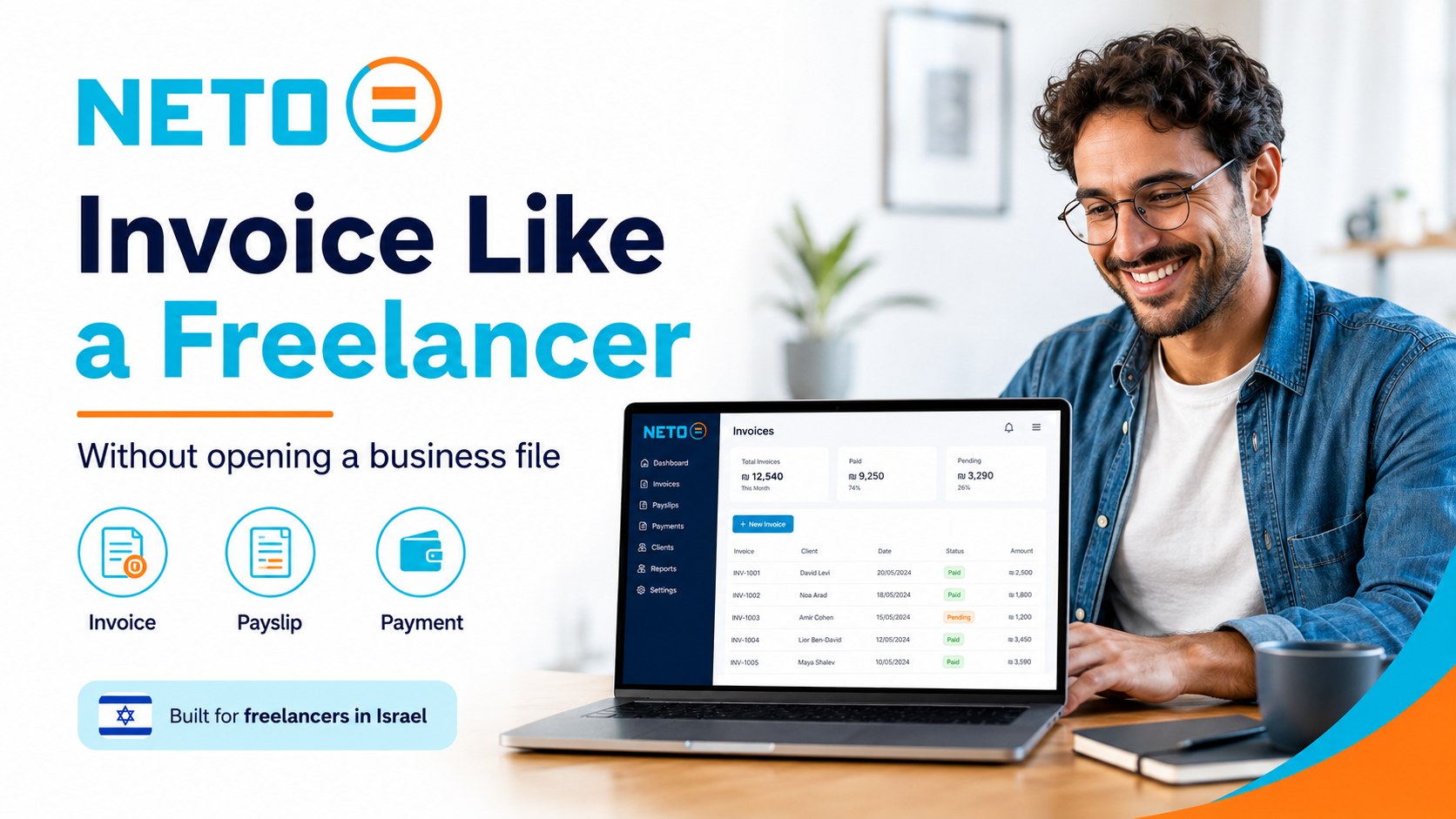

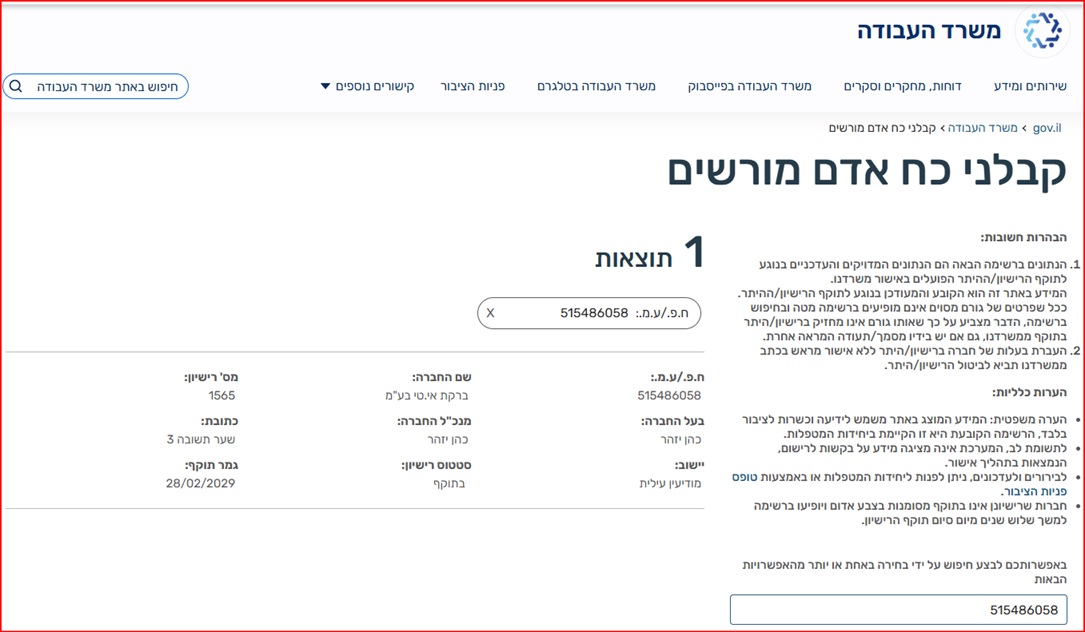

Work, issue a lawful invoice and get a proper payslip through a licensed manpower contractor (license 1565) · the deductions, reports and rights are handled for you as the law requires. NETO's fee is 5% taken from the client's pre-VAT invoice · you never pay it.

For a salaried worker, National Insurance and health contributions are deducted at source from the payslip · they don't need to open a file, file reports or remember deadlines. A self-employed person, by contrast, manages these payments themselves with the National Insurance Institute.

This is exactly where the NETO model works: anyone working as a freelancer or on a side income through NETO receives payment on a proper payslip · so the lawful deductions, including National Insurance and health contributions, are handled at source just as for any salaried employee, without opening a tax file and without bookkeeping. You can get paid by invoice as a salaried worker or use the NETO freelance payroll solution, and see how an invoice compares with a payslip.

NETO's fee is a simple 5%, taken from the client's invoice before VAT · the worker never pays it. NETO is operated by Bareket IT Ltd (company no. 515486058), a licensed manpower contractor under license 1565 supervised by the Ministry of Labor · and it upholds every one of your employee rights and mandatory benefits.

Everything stated above is neither advice nor authoritative reference · it is advisable to consult a professional such as a payroll controller, tax advisor, or attorney specializing in labor law. You are also welcome to reach our support and customer service · +972-8-976-1874.

On the NETO site you'll find a hub of further regulations, orders and laws · each link opens a full information page.

Every salaried employee in Israel pays National Insurance and health contributions from every payslip and on all income. The deduction is taken at source from the gross wage across two rates (2026 figures): 4.27% up to ILS 7,703 and 12.17% above · and anyone working through NETO gets a payslip where everything is already deducted and reported lawfully.

NETO lets you work and issue a lawful invoice · without opening a tax file and without the hassle with National Insurance, which is deducted at source on your payslip. Fast, free signup · NETO's fee is 5% from the client's pre-VAT invoice.

How National Insurance defines each · the brackets, the criteria and what it means for you.

Read more

Pension, leave, sick pay and a proper payslip · what every salaried worker is entitled to.

Read more

Worked two jobs and paid National Insurance twice? How to check if a refund is due.

Read more

The lawful way to invoice a client without opening a business · how it works.

Read more

The benefits a salaried worker in Israel is entitled to by law · the full list.

Read more

Earn a side income alongside your salary · lawfully, on a payslip, through NETO.

Read more

The difference between an invoice and a payslip · and which one is right for you.

Read moreHow National Insurance defines each · the brackets, the criteria and what it means for you.

Read morePension, leave, sick pay and a proper payslip · what every salaried worker is entitled to.

Read moreWorked two jobs and paid National Insurance twice? How to check if a refund is due.

Read moreThe lawful way to invoice a client without opening a business · how it works.

Read moreThe benefits a salaried worker in Israel is entitled to by law · the full list.

Read more YC

YCEvery section, organized by topic. Browse the full hierarchy or jump straight in.

Adjust the site to your needs

We use cookies to run the site and, with your consent, to measure traffic and improve your experience. Privacy policy

Barkat I.T Ltd · trading as NETO · is a licensed manpower company (license 1565), supervised by the Israeli Ministry of Labor.

Verify the license on the Ministry of Labor website

Full details · Manpower contractor license page →

Verify the license on the Ministry of Labor website

Full details · Manpower contractor license page →