Employer of Record Israel

Hire and pay staff in Israel without opening a local entity · NETO is the legal employer under license 1565.

Read moreLog in to your account, or sign up in a minute.

Pick whatever works for you · we're here.

Everything about NETO · transparent and available

Pick a convenient time · we'll confirm by phone/email

How US and EU companies grant equity to Israeli employees on the 25% capital-gains track under Section 102(b) · instead of the ordinary-income default.

Section 102 of the Israeli Income Tax Ordinance lets Israeli employees pay a flat 25% capital-gains tax on stock-option or RSU proceeds, instead of the ordinary marginal rate of up to 50% plus Bituach Leumi (National Insurance), which together can reach roughly 62%.

To qualify, the grant must run through an ITA-approved Israeli trustee on the Section 102(b) capital-gains track, the shares must be held by the trustee for at least 24 months from the grant date, and the plan must be filed with the Israel Tax Authority (ITA) at least 30 days before any grant. Foreign parents whose US ISO or RSU plans were never adapted to Israeli law usually default to the ordinary track and lose the benefit. NETO coordinates Section 102 grants together with an Israeli trustee under manpower license 1565.

If you are a US or EU company hiring engineers in Israel, your equity plan needs an Israeli overlay. This guide walks through why the US plan does not port over, the three tracks available, the trustee and the 24-month rule, ITA filing, vesting, and how NETO coordinates it all.

Reading time: 8 minutes · Focus: Section 102 Israel · Updated 2026

If you're a US or EU company hiring engineers in Israel, your existing equity plan was almost certainly drafted under US tax code · Sections 422 (ISO), 409A (deferred comp), and 83(b) elections. None of those map onto Israeli tax law.

Here's what happens if you just hand an Israeli employee the same US grant agreement your American hires get:

Section 102 of the Israeli Income Tax Ordinance exists specifically to solve this. It carves out a separate regime for employee equity and · when used correctly · drops the employee's tax to a flat 25% capital-gains rate. But you have to opt in through paperwork filed with the Israel Tax Authority before the grant. Retroactive fixes are not possible.

Israeli tax law gives a foreign employer three realistic tracks for granting equity to an Israeli employee. The choice determines the tax rate the employee pays · and the employer's obligations.

| Track | Who it's for | Employee tax | Trustee? | Holding period |

|---|---|---|---|---|

| Section 3(i) | Contractors, consultants, anyone who is not an employee | Ordinary income, up to 50% plus Bituach Leumi | No | None |

| Section 102(a) · ordinary track | Employees, when the employer wants to deduct the cost | Ordinary income at exercise | Yes | 12 months |

| Section 102(b) · capital-gains track | Employees, optimized for the employee | 25% flat capital gains | Yes (mandatory) | 24 months from grant |

For most foreign companies hiring Israeli employees, the Section 102(b) capital-gains track is the right answer. The employer gives up the ability to deduct the option expense for Israeli corporate tax purposes · irrelevant if you don't have an Israeli entity anyway · and the employee pays a flat 25%. Section 102(a) is mostly used by Israeli-incorporated companies that want the expense deduction.

Section 3(i) is the default that applies automatically if you ignore Section 102. It's also the only track available for contractors. If you're working with someone classified as a contractor in Israel · see our employee vs contractor test · equity grants will land in Section 3(i) and get taxed as ordinary income.

Section 102 makes the trustee non-negotiable. Without an Israeli trustee, the grant does not qualify · full stop. This is the single most common reason foreign companies miss out on the capital-gains rate: they assume their US transfer agent or a cap-table tool counts as a trustee. It does not.

An Israeli Section 102 trustee is a regulated role. The trustee must be approved by the Israel Tax Authority and is usually one of a small number of Israeli law firms or trust companies that specialize in employee equity. Their job:

The trustee fee is typically a setup charge per plan plus a small per-employee annual fee · trivial compared to the tax delta on a single liquidity event.

Here's the rule that catches the most companies by surprise: to get the 25% capital-gains rate, the trustee must hold the underlying shares for at least 24 months from the date of the grant · not from the date of exercise, and not from the date of vesting.

That distinction matters. In the US, the ISO clock for long-term capital gains starts at exercise. In Israel, the Section 102(b) clock starts at grant. So an Israeli employee granted options on Jan 1, 2026, who vests them on Jan 1, 2030, and exercises and sells on Jan 1, 2031, comfortably clears the 24 months and qualifies for 25%.

But an employee granted options on Jan 1, 2026, who exercises and sells within the same 24-month window · say in a quick acquisition in late 2026 · does not qualify. The proceeds get taxed as ordinary income under Section 102(a), even though the plan was filed on the capital-gains track. The 24-month rule is hard. The ITA does not bend it.

This is why founders who anticipate an acquisition need to file the Section 102 plan as early as possible · ideally at the company's first Israeli hire, even before there are real shares to grant. The clock can only start once the plan is filed.

Filing a Section 102 plan with the Israel Tax Authority is paperwork, not a discretionary review. There's no approval to wait for · the ITA accepts the filing and the plan becomes effective on a defined date. But the filing must happen at least 30 days before any grant is made under the plan. If you grant options first and try to file the plan afterward, those specific grants fall back to Section 3(i) or 102(a) by default.

The filing package typically includes:

Timeline from kickoff to a filed plan is realistically 4-6 weeks: 1-2 weeks for the Israeli trustee and Israeli employment counsel to draft the appendix, 1 week for board approval, plus the mandatory 30-day waiting period before the first grant. Plan accordingly if you've already promised options to a new hire.

Standard Silicon Valley vesting terms · 4 years with a 1-year cliff, monthly vesting after that · are fully compatible with Section 102(b). Israeli tax law doesn't care about vesting schedules; it cares about the grant date and the 24-month holding period at the trustee level.

Acceleration provisions also work, with one nuance worth flagging:

For exit planning, the practical advice is to grant the Israeli team as early as possible so that by the time a real liquidity event happens, the 24-month clock has long since cleared.

NETO operates as the Employer of Record (EOR) for foreign companies hiring in Israel · we hold license 1565 from the Israeli Ministry of Labor and run payroll for the Israeli employee under our entity, so the foreign parent doesn't need to incorporate in Israel.

Section 102 sits adjacent to payroll, not inside it: equity is granted by the foreign parent (the issuer of the shares), not by NETO. But the two pieces have to be coordinated · the trustee needs to know what's happening at payroll, and payroll needs to report option-exercise events correctly to Bituach Leumi and the ITA.

The foreign parent files the Section 102 plan with the ITA through our trustee partner, an ITA-approved Israeli trustee. Usual timeline: 4-6 weeks.

The grant is recorded with the trustee and the 24-month clock starts.

NETO's payroll engine flags the employee as having a Section 102 grant, so any exercise event triggers the right reporting and not double withholding.

When the employee sells, the trustee withholds 25% and remits it to the ITA. The payslip shows nothing · the gain is outside payroll.

For a foreign company hiring its first 1-12 Israeli employees, this is usually the cleanest path: NETO under license 1565 handles the employment relationship and payroll compliance, the trustee handles Section 102, and the founder only signs documents.

Related reading: how to hire Israeli employees · mandatory benefits in Israel · Israel payroll for foreign companies.

How NETO supports foreign employers hiring in Israel.

Hire and pay staff in Israel without opening a local entity · NETO is the legal employer under license 1565.

Read moreThe practical path for a foreign company to onboard its first Israeli hires, compliantly.

Read moreWhere to find engineers, how equity fits in, and how to employ them without a subsidiary.

Read morePension, severance, recreation pay and the statutory benefits every Israeli employee receives.

Read moreCompliant monthly payroll · payslips, National Insurance and pension calculated correctly.

Read moreWhat it really costs to employ someone in Israel, from gross salary to statutory add-ons.

Read moreSection 102(b) turns a potential 62% tax bill into a flat 25% for your Israeli team · but only if the plan is filed with the ITA, a regulated Israeli trustee holds the shares, and the 24-month clock has run from the grant date. Get the paperwork in early, and the tax efficiency is there when a liquidity event arrives. NETO coordinates the employment, payroll and trustee side so the founder only signs documents.

NETO coordinates Section 102 filings with our trustee partner, so the 25% capital-gains track is locked in from day one · not retrofitted after the exit.

YC

YCEvery section, organized by topic. Browse the full hierarchy or jump straight in.

Adjust the site to your needs

We use cookies to run the site and, with your consent, to measure traffic and improve your experience. Privacy policy

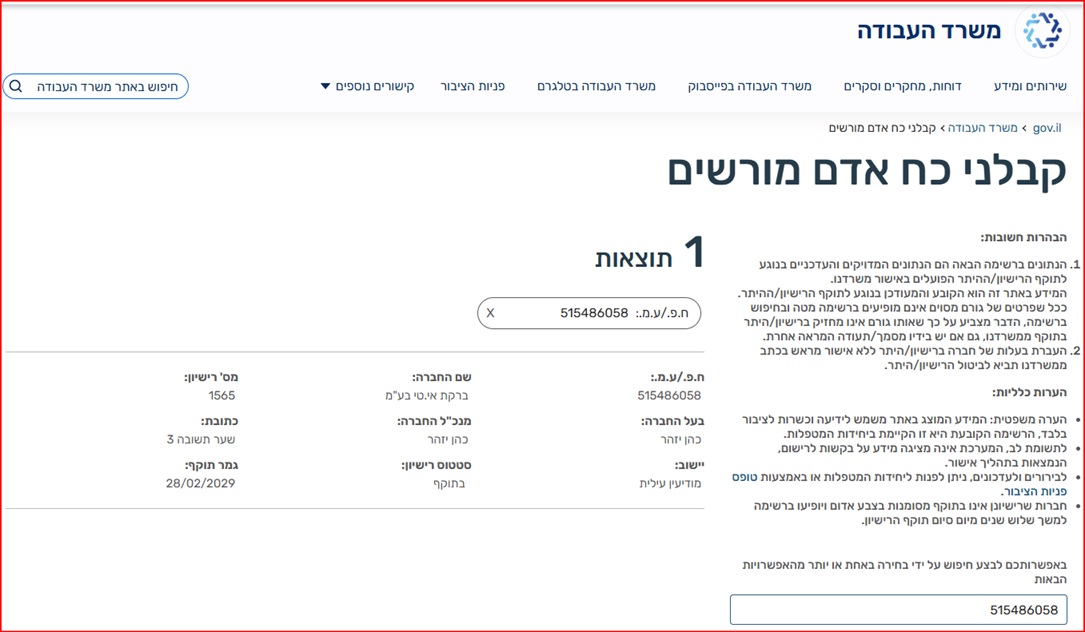

Barkat I.T Ltd · trading as NETO · is a licensed manpower company (license 1565), supervised by the Israeli Ministry of Labor.

Verify the license on the Ministry of Labor website

Full details · Manpower contractor license page →

Verify the license on the Ministry of Labor website

Full details · Manpower contractor license page →